- 1 All About Discounted Cash Flow Method {DCF}

- 1.1 Meaning of Discounted Cash Flow Method {DCF}

- 1.2 What a Discounted Cash Flow Method {DCF} works

- 1.3 Need of Discounted Cash Flow Method {DCF}

- 1.4 Advantages of Discounted Cash Flow Method {DCF}

- 1.5 Help to find real/ intrinsic value of investment

- 1.6 Disadvantage of Discounted Cash Flow Method {DCF} –

- 1.7 Difference between Discounted Cash Flow Method {DCF} and NPV

- 1.8 Steps involved in Calculation of DCF

- 1.9 Calculation of Discount Rate

- 1.10 Calculation of Terminal Value

- 1.11 Calculation of Present value {PV} of future cash flows

- 1.12 Calculation of share price

- 1.13 Value of each share

All About Discounted Cash Flow Method {DCF}

Meaning of Discounted Cash Flow Method {DCF}

Discounted Cash Flow Method {DCF} is performed by different entities {Likes – investors, businessmen, management etc.). Discounted Cash Flow Method {DCF} basically use to evaluate investments and help to get valuation of different companies. This method calculates precise price of any company share or value of any other security.

What a Discounted Cash Flow Method {DCF} works

Discounted Cash Flow Method {DCF} is basically predict / estimate all possible cash flows will be generated by company in the future and calculate its worth in present time by using Discount rate [r}. Simply DCF analysis estimate future performance of a company based on the historical data and calculate its value in the present.

After all the assumptions and forecasting an investor calculate the intrinsic value of the company according to current situation. {You have to basic knowledge of Time Value of money} {Click here– TVM}

Need of Discounted Cash Flow Method {DCF}

Discounted Cash Flow Method {DCF} is very reliable for valuation of companies. Compare to other analysis methods {Because this analysis urge that a company will operate in the long term} So according to this assumptions DCF method is widely used for valuation because under DCF analysis it accumulates all future cash flows of the company {Based on assumptions and according to historical data} and calculate its present valuation by using Discount rate.

Advantages of Discounted Cash Flow Method {DCF}

Diversified Usefulness

Discounted Cash Flow Method {DCF} is highly useful in different ways. Because DCF is not only reliable for Company valuation but also it is highly useful for evaluating business projects or investment purposes. DCF estimate whether the investment is reasonable for investors and generate enough profits or not.

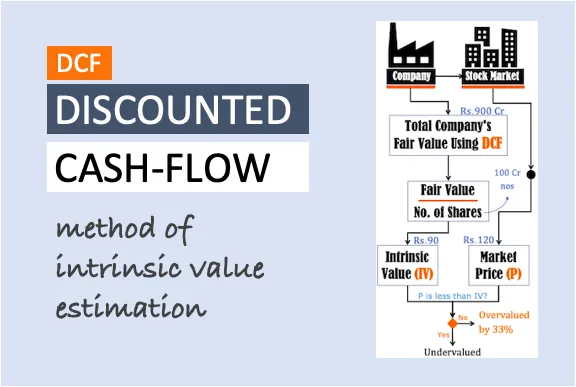

Help to find real/ intrinsic value of investment

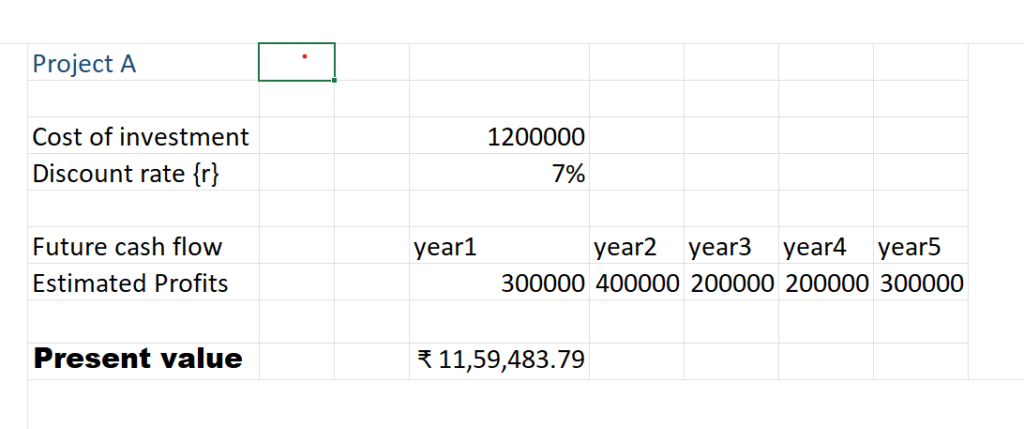

Through its reliable mechanism Discounted Cash Flow Method {DCF} is estimate all future cash flows and calculate its present worth means it give us what the actual value of investment in present time {Calculate Intrinsic Value} and show whether the share or investment cost is reasonable or not. Let us take an example to understand how Discounted Cash Flow Method {DCF} is used –

- If you focus on the above example than you analyze the present worth of the Project A is approx. 11.5 lakhs, but it cost of 12 lakhs, so this investment is not profitable. / Reasonable for the investor by this way DCF is highly useful to evaluate different projects or investments.

Adjustable Scenarios

Discounted Cash Flow Method {DCF} is highly used by investors because of its working mechanism it shows quickly how different types of conditions, scenarios and very important it display how effectively future cash flows affected through all by these circumstances and which company cash flows respond according to it.

Disadvantage of Discounted Cash Flow Method {DCF} –

Involve too Many Assumptions

Under Discounted Cash Flow Method {DCF} analysis an investor has estimate too much like if they forecast for next 5 years so they have to estimate company 5 years financial statement, their growth, financial soundness and all factors that may be affect the company that involve high chances of wrong assumptions that may be backfire in the future. Hence leads to wrong valuation by which there is a higher chance that investor cannot achieve its expectations.

Unknown Economic and other changes

When an investor makes assumptions under Discounted Cash Flow Method {DCF} then he may not consider many factors {like – Government policies, business environment, changes in technology, level of competition etc.} that has huge impact on the target company because a company cannot operate in isolation, so theses’ unknown economic factors also affect company future cash flows, growth and their potential.

Risk of false Assumptions

Under Discounted Cash Flow Method {DCF} we already know that under its mechanism we have to estimate many things and that make DCF model risky and fill with lots of uncertainty because if an investor failed to predict company future by a big margin {Because no one predict accurately} then this cause wrong valuation and maybe he does not gain his expected returns that leads to discourage its future investments.

Difference between Discounted Cash Flow Method {DCF} and NPV

Major difference is DCF is not exclude the initial investment, but NPV does. DCF is used to calculate either the investment is worthful or not on the other hand NPV calculate profitability of any project based on expectations Set by the management {According to WACC calculation and Expected cash flows} NPV only assume expected returns, but DCF forecast not only company and its financial but also estimate other factors for calculation. DCF analysis mechanism help to find out any investment intrinsic value and shows either the investment is overvalued or undervalued whereas NPV only display that the specific project meets management expectations or not.

Steps involved in Calculation of DCF

Estimate Future Cash Flows –

This is the first step under this first of all an investor has to estimate future cash flows of company and forecast its financial soundness for Discounted Cash Flow Method {DCF} for this estimation first we have to determine for how many years we want to forecast company cashflows. But it is not easy it is a lengthy and bit complicated process because we have to prepared financial statement and predict financial soundness of the company in the future for cash flow estimations.

- Let us discuss how to predict future financial statement in deep to understand it clearly-

Forecasting Income statement {P&L Statement}

First of all, we have to forecast Income statement for calculation of free cash flow under DCF Model. Under this we estimate company future gross profit, all type of expenses, tax rate, net profit and all types of non-cash items.

Things must take into consideration for forecasting revenue –

- If a company operate in multiple countries like big firms does, they some of them display their separate Income statement on regional basis if any company do it so its Income statement forecast also done on regional basis {like growth rate in a particular region}. For example – Coco- cola disclose his income statement on regional basis.

- Only organic growth should be included for Forecasting Income statement because only organic growth is the real growth in the long term, and it recurred regularly in future, and it make our predications more accurate and give a realistic number. Organic growth like – Increase geographical areas, increase sales volume and increase product chain.

- Inorganic growth / Extraordinary items should not be included in the Forecasting Income statement because this are non-recurring in nature and maybe not occurred in the near future it also makes our predications wrong and calculate an unrealistic number.

Factors affecting Income statement Forecasting –

- First of all, understanding nature of business and company revenue model is essential. If company operates in Real estate industry, then it is highly volatile in nature compared to pharma industry which are steady in nature or if a company revenue model focus on one time sale so its revenue is generally lower than the Subscription based revenue model company.

- If company operate in emerging market so it has high potenyial to grow

- If company used new technology then also make company more efficient hence revenue also increase

- If company has Patents of some special technology to make company more effiecent and give an extra compatative edge than it als increase company growth potential

- If company has high qualified management and team so it also affects company growth.

- If company has exclusive product so it also increases company earning capacity.

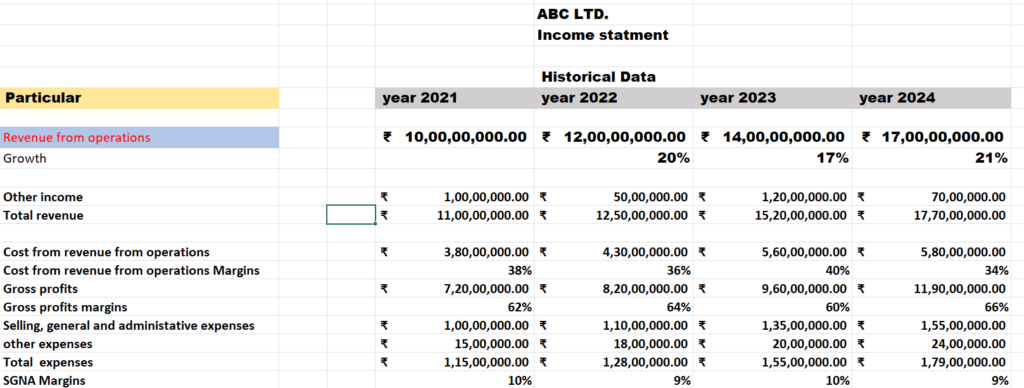

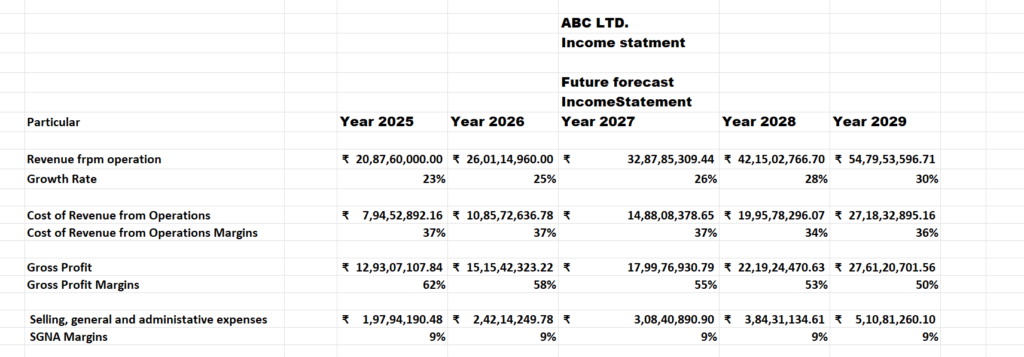

- Let us take an example to understand how to forecast Income statement –

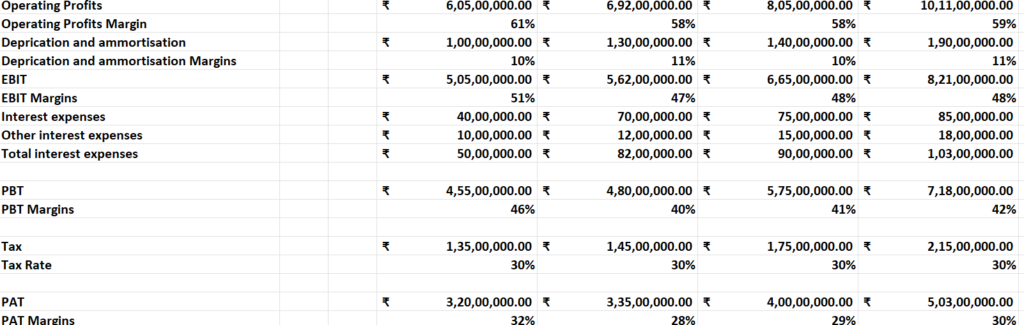

- If you observe the above diagram, then you understand that first of all we analysis ABC LTD. historical data and drawn some conclusion and express them mathematically to used them more efficiently than we prepare last 4 years Income statement to forecast their future Income statement.

- Things you considered before analysis of the example –

- In the DCF analysis we include other income in the calculation of The Total income of previous years, but we should not include them in the forecasting process because other income is non-recurring in nature so it hard to predict and make Discounted Cash Flow Method {DCF} calculation wrong.

- Same goes to other expenses because other expenses also non-recurring in nature so it hard to predict them also and make Discounted Cash Flow Method {DCF} calculation wrong.

- We calculate Growth / Margins of different important terms, so we predict future income of the company more easily.

- Now Forecast the Income Statement –

- As you can see and analyze that in the above diagram, we forecast future income statement {Based on historical data and estimations} now let us discuss important terms in detail that how we can forecast them –

Revenue From Operations

This is one of the most important parts of Income statement this display that how much company able to sale its product and services, what is their average Revenue and shows their sales volume simply it shows the total revenue generated by the company through sales.

- Points took considered for forecasting –

- If you analyze above diagram then you notice we calculate revenue growth of the company then we assume growth range in which company revenue may increase {Based on information of Market, Company Position, Company goodwill among customers}

- Same goes to Cost of Revenue from Operations we calculate its growth through Average method {because its growth is fluctuated and also move in a certain range}. and estimate future Cost of Revenue from Operations

- Then we forecasted Gross Profit through predicted Revenue from Operations and Cost of Revenue from Operations to estimate what is company Gross margins and gross profits.

- Important Formulas –

- Gross Profits = {Revenue from Operations – Cost of Revenue from Operations} / Revenue from Operations * 100

- Growth Rate = Y1 – Y0 / Y0 *100

Here –

- Y1 = Next year after initial year

- Y0 = Initial Year

Selling, General and Administrative Expenses

- These all are operating expenses that occurred on the regular basis due to carry out business operations and activities. These show where company spend his revenues for business operations, distribution of revenue among different operating expenses.

- Point to considered to forecast Selling, General and Administrative Expenses –

- First, we use historical data and calculate its growth through Average method because it also moves in a certain range and then use those Growth rate to estimate future SGNA expenses.

- Important Formula –

- SGNA growth rate = Average of past years SGNA expenses/n

- n = Number of years used for calculation

- Calculation of SGNA expenses through Growth Rate –

Percentage {%} growth of SGNA Expenses * Revenue from Operations

Operating profit

These is a crucial element to understand how efficiently a company carry out his operations and business activities because it excludes all type of operating expenses. If company has high operating profit than it means company is highly efficient and if not, then company have to focus on its process to become more efficient. Operating profit display how efficiently company utilize its business operating expenses to minimize wastage of revenue.

- Point to considered for estimation of future operating profit –

- Simply we use Average method because it moves in a range that you can see in the historical data diagram, and we calculate operating profit through excluding future SGNA Expenses that we forecasted earlier.

- Important formulas –

- Operating Profit = (Gross profit – SGNA Expenses) / Revenue from Operations * 100

Deprecation and Amortization

Deprecation is a normal and continuous phenomenon that leads to decrement in the value of tangible assets due to regular usage, normal wear and tear and due to accident. Amortizations is decrescent in value of intangible assets on regular basis due to passes of time.

- Point to considered for estimation of future Depreciation and Amortization –

- For calculation of future Deprecation and Amortizations we calculate its growth range, but Deprecation and Amortizations is used on assets, and we cannot predict accurately that how much assets company acquire in future and how much it will grow up, so we use a constant rate to maintain a realistic approach.

Earnings before Interest and Taxes {EBIT}

This show how much revenue company will be held before paying interest on its debts and cooperates tax. This also show how much company used its revenue to paying interest of its debt. Through Earnings before Interest and Taxes {EBIT} we estimate company earning and growth capacity because taxes are not under control of company, and it bit similar for interest because debts are essential to grow businesses.

- Point to considered for estimation of future Earnings before Interest and Taxes {EBIT} –

- For calculation of EBIT, we first exclude Deprecations and Amortizations that we calculate earlier, and we calculate its growth rate through Average method.

- Important Formulas –

EBIT = EBITDA – Deprecations and Amortizations / Revenue from operations * 100

- EBITDA = Earnings before Interest, Tax, Deprecations and Amortizations

- Profit before Tax {PBT} – At this stage the only cost is left for the business is to pay cooperate tax

- Important Formulas –

PBT = EBIT – Tax / Revenue From Operations * 100

- Profit After Tax / Net Profit {PAT} – This is the net revenue or profits that are generated by the company after subtracting all its obligations.

- Important Formulas –

PAT = PBT – tax / Revenue From Operations * 100

Calculation of Free Cash Flow to Firm {FCFF} –

EBIT *{1 – tax rate} / NOPAT + Non-Cash Item +/- Change in Working Capital – Capex on Plant & Equipment

Calculation of Discount Rate

It is very important to calculate because it used to discount all Future Cash flows {generated by company} to calculate their worth in present time, simply this discount rate is used to calculate all future cash flow present value. {You should know about Time Value of Money).

For this purpose, we used WACC Method for Discounting Purpose.

- I already explain all about WACC {click now – WACC to understand it easiest way} but take a quick summary like how to calculate Cost of Debt and Cost of Equity for WACC –

Methods to Calculate Cost Of Debt –

Based on Historical Data –

Sometime company calculate its Cost of Debt on the basis of past because it not too much complicated and company easily calculate its Cost of Debt.

- Important requirement for this method –

- Company has taken lots of Debt from the Financial institutions

- They have to borrow funds in the recent past so data is more realistic and estimation make more accurate.

Bond Yield Method

Some investors calculate a company Cost of Debt on the basis of Government bonds / Treasury bills. Because Government bonds / Treasury bills is the safest place to invest {Government bonds / Treasury bills have almost neglected default risk}. So, through this investor calculate on basis of those interest rate provided on bonds to calculate more realistic number.

Risk Based Method

Some investors or even banks also use this method before providing loans to a company. In this method first of all banks calculate its opportunity cost {Means if banks invest their money somewhere else like in government securities} in other words Risk free returns {RF} and also considered company default risk {Credit worthiness} through their Credit Score {like – AAA, AA et}

- Formula –

RF + x = KD

- x = Additional risk bear by the company

- RF = Risk Free Returns

- KD = Cost of Debt

Method to calculate Cost of Equity {KE}

there is a method which is most commonly and widely used by all types of investors to Calculate Cost of Equity {KE} and that is CAP Model {This describes to limit or range in which a investor should expect from a particular share}

- Formula to Calculate CAP Model –

RF + beta {RM – RF}

- RM = Market expected returns

- Beta – Risk related to a particular Security.

- After calculating both Cost of Equity {KE} and Cost of Debt {KD} than you should multiply them with their weight in the company capital structure then you obtain WACC.

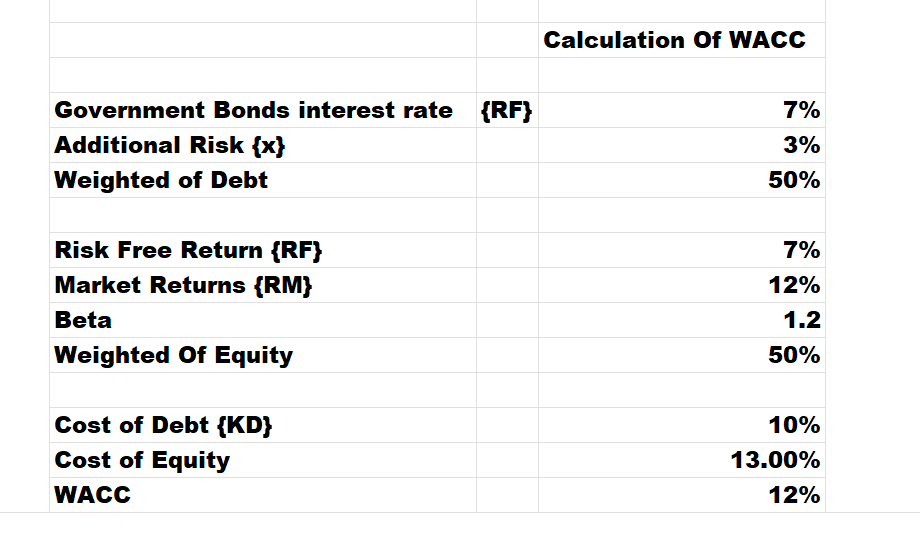

- Let us take an example to understand much better of WACC calculation –

- As you can see in the above example and if you analyze then you understand how we calculate WACC. Let us understand calculation –

- For Cost of Debt, we assume that company highly credit worth company, so we assume additional interest is 3%, so –

- Kd = Rf + x

- Kd = 7% + 3%

- Kd = 10%

- For calculation of Cost of Equity, we assume Beta will be 1.2 {Beta calculated systematic, but I already explained in previous blog}. For Risk free return we take 7% because you can this return easily on FD and Nifty returns for past 10 years was 12%.

Ke = Rf + Beta {Rm – Rf}

Ke= 7% + 1.2*{12% – 7%}

Ke= 13%

- When you calculate both Cost of Equity and Cost of Debt then you easily calculate WACC through

- WACC = {Kd * Weighted of Debt} + {Ke * Weighted of Equity}

- = {10% * 50%} + {13% * 50%)

- = 12%

Calculation of Terminal Value

Even if we forecast a certain time range of a company it cannot be sufficient to valuate a company because according to Going Concern Concept. A company run for a very long time, so it is important to calculate its all-possible future cash flows {Based on recent data and some assumptions} for this we use a certain formula –

Terminal value = FCF1 / WACC – g

- FCF1 = Next year cash flow after the last year of estimated / forecast year

- g = Growth rate of company

- Assumptions must be considered for Terminal value –

- After forecast period we assume that the company grow at the same rate their country GDP grow annually.

- We forecast next year based on previous year average growth rate.

| ABC. LTD. | |

| FCF0 | 100000000 |

| Growth rate of Cas flows | 10% |

| WACC | 12% |

| g | 7% |

- Terminal value = {10000000 * 10%} / {12% – 7%}

= 220 crores

- Calculated Terminal value is 220 crore means if we add all future cash flows after projection period so it equal to 220 crores.

Calculation of Present value {PV} of future cash flows

After we calculate all possible future cash flows, we have to convert them into present price means what is their worth in present time for this we use time value of money concept.

Let take an example to understand it much better –

| Cash flow of year 1 | 30000000 |

| Cash flow of year 2 | 50000000 |

| Cash flow of year 3 | 80000000 |

| Cash flow of year 4 | 90000000 |

| Cash flow of year 5 | 100000000 |

| Terminal value | 2200000000 |

| Discount rate | 13% |

- Present Value {PV} – Future value of cash flows / {1+ r}n

- = 2550000000/ {1 + 13%}

- = 128 crores {approx.}

- As you can understand the above table calculation, we simply calculate all possible future cash flow present value. These 128 crores is the value of the company in present time.

In these steps we divide current value of the company by number of outstanding shares of the company {Means number of shares currently floated in the market freely}.

- Basic things take to consideration for calculation of share price –

- First of all, exclude all claims of Debt holders

- Add cash & cash equalvent present in company balance sheet

- Add all investments performed by the company

- Formula to calculate Share Price –

Value of firm – Claims of Debt holder + Cash & Cash Equivalvent + Company investment / Number of company outstanding shares

- Let us take an example to understand it much better –

| ABC. LTD. | |

| Value of Firm | 128 crores |

| Claims of debt holder | 50 crores |

| Cash & Cash Equivalvent | 22 crores |

| Company investment | 30 crores |

| Number of company outstanding shares | 1 crore |

- Value of firm – Claims of Debt holder + Cash & Cash Equivalvent + Company investment / Number of company outstanding shares

= 128 – 50 + 22 + 30 / 1

= RS 130 / each share price

- That how all share price calculated by DCF Model