All About Time value of money

Introduction

All persons who have interest in finance they have first of all knowledge about Time value of money. If you see on internet there are numerous facts about investing. Like some people say if you invest there you make this sum total of money.

- Let me ask you a question what is the basis of their point? and the answer is Time value of money. let understand what Time value of money in detail.

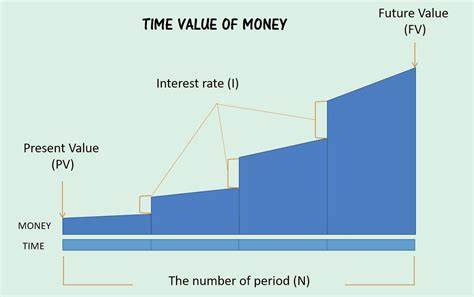

What is Time Value Of Money

The meaning of Time Value Of Money is that value of money that you held either in present or in future. Or how much do you invest today to get a certain amount in future.

- Simply Time Value Of Money is a type of scale that measure money on time basis.

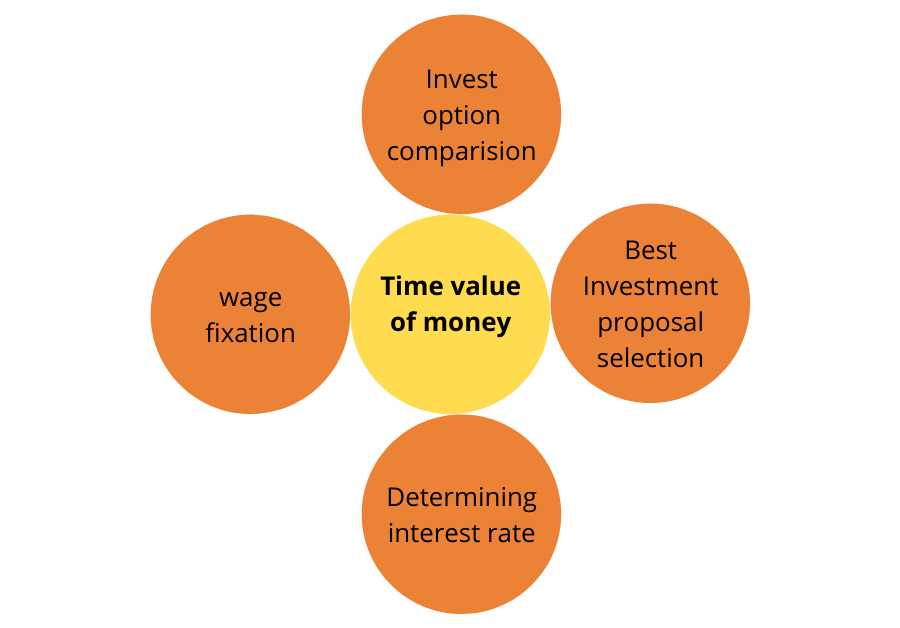

Reasons to use Time Value Of Money –

- For comparison of different investment ways

- To invest money to obtain maximum profits

- To evaluate different projects of business and their Rate of return

- To help management in decision making to evaluate different investment

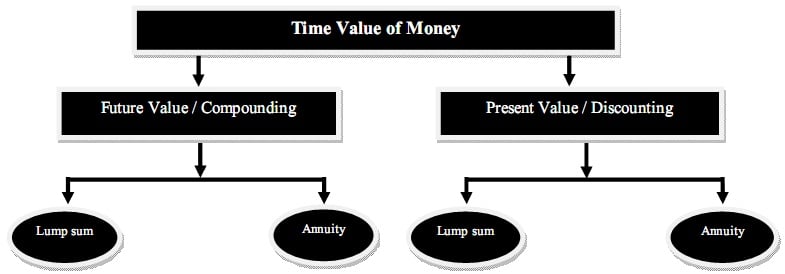

Basic terms you need to know before understanding Time Value Of Money

As you can see in the above chart of Time Value Of Money let us understand all one by one

- Discount rate (r) – This is the expected rate that investors or businessman expect to gain before investing in any project and this is an essential element in Time Value of Money because it used in calculation of PV and FV,

- Present value (PV) – Simply it is value of money that you held in present.

- Future value {FV} – This is the value of money that you obtain in future after investing the amount somewhere.

- Total investment time period {n} – This is the total time someone invested in a particular investment.

- Cost of capital – Sometime business does not have enough funds for running business, so they raise funds from market therefore they pay some cost for it {like interest on loan or dividend on shares} this is called cost of capital. Simply the additional cost occurred due to raise funds from market is called Cost of capital

Why Time Value Of Money needed –

- Due to Purchasing power and Inflation – We all know Purchasing power and Inflation are very important terms in our daily life Purchasing power and Inflation has a negative relations means with the time when inflation increase our purchasing power will decrease to overcome this situation Time Value of Money needed because it helps to invest in those areas where we maximize our money and our good Purchasing power.

Types of Time Value Of Money –

As you can see the above diagram, of Time Value Of Money let understand all its types in detail

Present value {PV}

As I explained above this value of money that you held today or the current value of your investment that you calculated from future perspective.

Present value {PV} of lumpsum

when you invest whole amount in a single investment for future return, so it is called Present value {PV} of lumpsum

- Formula of Present value {PV} of lumpsum =

PV = FV/ {1+ r} n

- FV – Future Value

- r – Rate

- n – Number of years invested

- Let us take an example to understand it much better –

Additional information –

- On yearly basis –

| Future Value {FV} | 100000 |

| Rate of Return | 7% |

| Invested Time | 5 Years |

- If you do it manually it looks like below equation

Present Value PV = 1000000/ {1+0.07}5 = 71299 {Approx}

As you can see in the above table the future Value of your investment of 1 lakh is currently has a value of 71299 {Approx} means if you invest 71299 {Approx} today you will get 1 lakh after 5 years on this investment. That is the simple means of Present Value PV.

Present value {PV} on annuity basis

When you invest multiple times in future then to calculate all investment present value we use Present value {PV}on annuity basis. To calculate what value they held in present time.

- Let us take an example to understand it much better –

| Future value | End of Year 1 | End of Year 2 |

| Regular Payment {P.A) | 10000 | 10000 |

| Discount rate | 7% | 7% |

So, its calculation –

- For year 1 – PV = 10000/ 1.07 = 9346 (Approx)

- For year 2 – PV = 10000/ 1.072 = 8734 (Approx)

Formula used – Future value / {1 + r} n

As you can see in the above example then you understand that you can calculate multiple years investment current time worth through PV.

Net Present Value {NPV} –

- Purpose of NPV –

- To evaluate company valuation

- To evaluate any business project worth either its profitable or not

- To evaluate any investment for its worth.

- Help management to evaluate and decision making for different projects.

- Requirements of NPV –

- Company cash outflow on the project

- Net cash inflow of the project in future

- Expected returns {Discount rate} decided by management.

- Things to remember of NPV –

- Terminal Cash Flow – IF in the future management decide to sell off the project, investment and business so it considered as Terminal Cash Flow.

- If NPV is negative so it’s not mean that it causes loss instead its means project is not able to meet management expected returns.

- Formula of NPV – FV/{1+r}0 + FV//{1+r}1 ……

- Let us take an example to understand it much better –

| Future value | End of Year 1 | End of Year 2 | End of Year 3 |

| Expected income | 100000 | 250000 | 300000 |

| Discount Rate | 15% | 15% | 15% |

- Additional information –

- Company XYZ want to run a project for 3 years and they expect income {mention above} and their expected returns is 12% and the amount will invest is 500000 and after that they sell it for 100000 at the end of third year.

CALCULATION

For first year – 100000/ {1 + 0.15} = 86957 {Approx}

For second year – 250000/ {1 + 0.15} 2 = 189036 {Approx}

For third year – 400000/ {1 + 0.15} 3 = 263006 {Approx}

Total amounts earn after time adjustment / NPV = Amount invested in project – Amount earn through project

= 500000 – 538999 = 38999 RS

It means this project is profitable for management and they should invest in this project. If this value is negative means this project is not able to meet management expected rate.

Future Value {FV}

This shows how much our investment in any project and business worth in the future from Present perspective.

Future value on Lumpsum –

Formula – FV = PV {1 + r} n (Yealy basis)

FV = PV {1 + r/12} n*12 ( Monthly basis)

FV = PV {1 + r/365} n*365 ( Daily basis)

- Let us take an example to understand it much better –

| Present Value {PV} | 100000 |

| Expected Rate | 7% |

| Time Period | 5 years |

Calculation of the above –

FV = 100000{1+ 0.07}5 = 140255 {Approx}

As you can see in the table, we calculate Future value of our investment of worth 1 lakh on yearly basis means what the worth of our investment of 1 lakh after 5 years.

Future value on Annuity basis {FVA}

When we do not invest whole amount in lumpsum instead we invest on regular basis like either on yearly or monthly basis. Then it called Future value on Annuity basis.

- Formula –

Future value of Annuity – A {(1 + r) n – 1 / r}

- Let us take an example to understand it much better –

| Future Value | Year 1 | Year 2 | Year 3 |

| Annuity | 100000 | 100000 | 100000 |

| Rate | 7% | 7% | 7% |

Calculation of this equation

FVA = 100000{ ( 1+ 0.07 )3 -1 / 0.07 = 321490 RS

As you can see in the above table that if you invest 1 lakh on yearly basis so it worth 3.21 lakhs after 3 years {If it compounds on Yearly basis} by this you can easily calculate any amount future value.

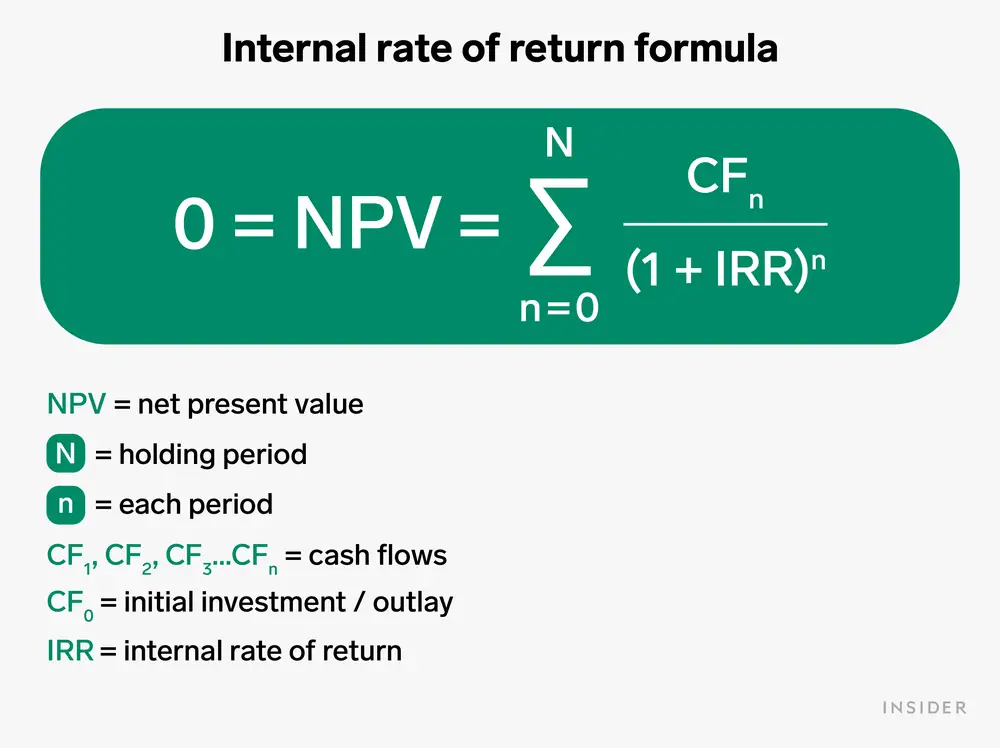

Internal rate of return {IRR}

This is a metric that help to understand about any project, business and investment profitability. In this discount rate of NPV is 0. Simply IRR help in to calculate annualized rate of return.

- Let us take an example to understand it much better –

| Future Value | Year 1 | Year2 |

| Amount received | -10000 {invested} | 120000 |

| Rate | 12% | 12% |

Calculation of the equation

- NPV = FV/{1+r}0 + FV//{1+r}

0 = -10000/ {1+0.12}0 + 12000{1 + r} 1

0 = -10000/1 + 12000 / {1 + r }1

After you simplified it so

10000 = 12000 / {1 + r }1

{1 + r }1 = 12000/10000

r = 0.2

So, IRR will be 20%

NPV VS IRR –

By the way both metrics are very crucial to calculate before investing in any project, business and investment because both measure profitability and evaluate whether management invest in them or not but sometime these both metrics show different results, and management wants to invest in only one then let us understand how to choose them.

- Circumstances that must be fulfilled –

- NPV must be Positive means it fulfill management expected returns.

- IRR must be more than cost of capital {Cost of capital explained above}

Let us take different situation to understand it much better

Project A

| Investment in project | 100000 |

| Expected return from project | 150000 |

| Discount Rate {r} | 7% |

| IRR | 50% |

| NPV | 37558 (Approx) |

Project B

| Future Value | Year 1 | Year 2 | Year 3 |

| Expected return | 350000 | 0 | 0 |

| Discount rate | 7% | 7% | 7% |

| IRR = 33% | |||

| NPV = 126826 {Approx} | |||

- Additional information

Investment made by the management in Project B is 150000

As you can see in both the projects in project A IRR is very high around 50% whereas in Project B NPV is higher than the IRR and if company want to invest in only one project so management should prioritize NPV over IRR because NPV show actual return come from investment.